Gladiators, ready! Pricing models fight it out

Nonplussed by neural networks? Intimidated by the jargon? You can’t afford to

be, not in the fast-paced pricing arena. Four actuaries put two cutting-edge

models to the test, to see which wins out.

In the competitive world of pricing, actuaries are racing to deliver greater accuracy in

smaller timeframes – and a host of new and increasingly sophisticated modelling

architectures can be used to gain that elusive edge.

Here, we describe and test two of these modelling technologies, the combined

actuarial neural network and the LocalGLMnet, which use classical statistical

methods alongside neural networks to improve predictive accuracy. Every second

and penny counts; used wisely, these solutions may present an advantage.

Putting it simply

Neural networks can seem intimidating, with the terminology around these models

no doubt contributing to this. The jargon, with its neurons, activation functions and

layers, can sound foreboding at first – but don’t let it scare you off. Let’s demystify

the nuts and bolts of neural network architecture.

To draw from common actuarial and statistical knowledge, we can think of a neuron

as a univariate binomial generalised linear model (GLM). In this simple case, the

activation function is the logistic function. If we were building a GLM, we would be

nearly finished, but a neural network consists of several such GLMs working

together. How? Each neuron calculates a single number, and a collection of these

form a layer. There are two mandatory layers (the input and output); any layers in

between are referred to as hidden layers. The number of neurons in a layer, and the

number of layers in the neural network, can be set manually or through a tuning

process.

The first (input) layer consists of our predictors, which are then passed to neurons in

the first hidden layer. Inside each neuron, the inputs are scaled and shifted by

weights and biases before feeding through the activation function. After these

calculations we obtain an output of the first hidden layer, which is then passed to the

second layer, and so on, until we reach the network’s output layer. When information

flows in this forward direction, from input layers to output layers, the model is known

as a feedforward neural network (FFNN).

Why do we say neural networks are trained, or learn? As a comparison, when fitting

a linear regression model, numerical techniques are used to converge on a solution to a closed-form problem. In neural networks, however, there are so many model parameters and so many intractable interactions between them that such closed-form formula does not exist. We use iterative optimisation techniques to tweak randomly initiated parameters until they produce an output close to the given target

variable.

Combined actuarial neural networks

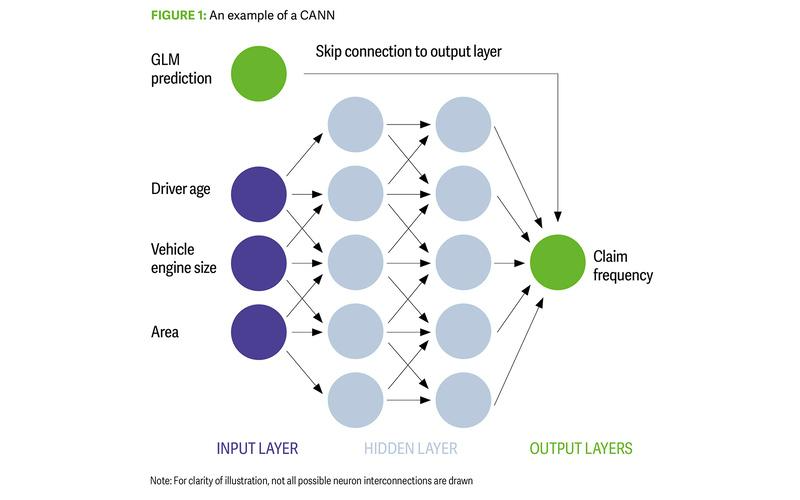

A combined actuarial neural network (CANN) embeds a GLM into a neural network

using a skip connection that directly links the input layer to the output layer (Figure

1).

It is essentially a neural network that uses the benchmark GLM’s predictions while

learning additional interactions among variables to improve the overall model’s

predictive power. There are three common approaches to using a CANN:

- The GLM element is non-trainable, so the benchmark GLM is always

present and only the network part changes. This is the form of CANN included

in the analysis to follow. - The entire network parameter can be trained, meaning the benchmark

GLM can be modified. - A trainable credibility weighting can be introduced for the fixed GLM

element within the CANN.

While CANN may not generally outperform pure neural networks in minimising the

objective loss function, its value for pricing teams lies in uncovering nuanced

interactions that can enhance existing GLMs in production.

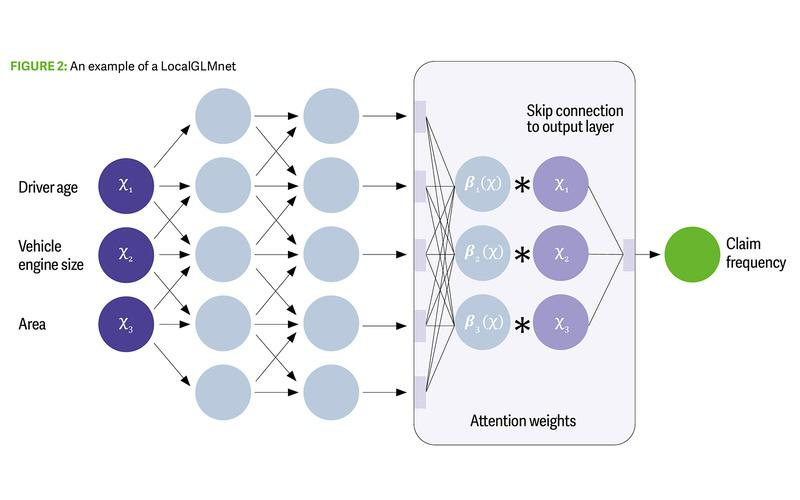

LocalGLMnet

This structure predicts GLM’s coefficients for each individual record using a neural

network, leveraging the GLM’s advantages in terms of explainability. However, it

gains predictive accuracy by allowing the coefficients to vary for each record. The

LocalGLMnet uses a skip connection (different from that used in the CANN), directly

linking the input features to the output layer. This provides a linear term in the model,

which bypasses the neural network, and then weights these terms with potentially

non-linear weights.

Successfully training this neural network leaves us with a highly predictive model and

a set of beta coefficients (attention weights) for each observation (Figure 2). Now we

can interpret the prediction in a familiar way but also analyse the attention weights

and how they vary for different predictors.

Results

Now that we have conceptually described these two new models, let’s road-test

them and see how they perform on real-world data. In this case, we use them to

predict the frequency of third-party motor liability claims for individual customers,

using a publicly available dataset with 680,000 records and 11 features relating to

motor policies of a French insurer. This dataset is commonly used in literature on

actuarial models and model benchmarking.

We studied CANN and LocalGLMnet and included the GLM and FFNN models for

comparison. A simple intercept model is also included for reference. A full

description of the implemented models is beyond the scope of this article, so we will

focus on high-level results and conclusions from the exercise. A more detailed

presentation of this work will be available in an accompanying blog post on Towards

Data Science and a GitHub repository (github.com/Karol-

Gawlowski/ADSWP_NN ).

Every second and every penny counts; used wisely, these solutions may present an advantage

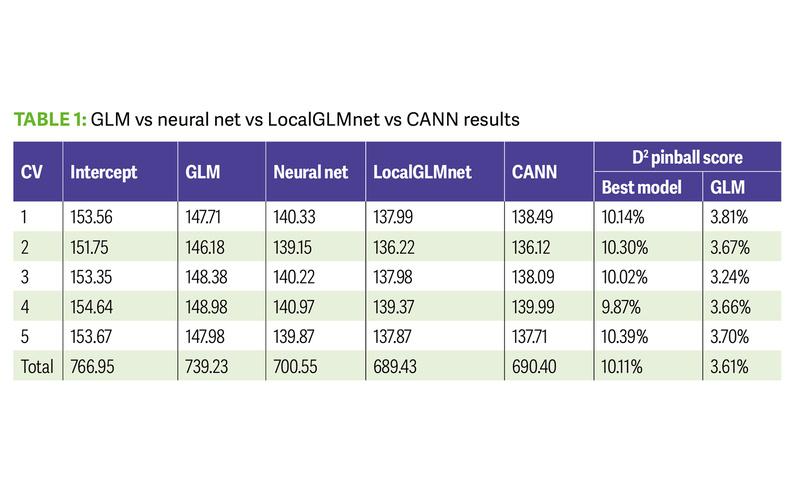

Table 1 shows the results of a cross-validation (CV) exercise over five folds of the

data. In a five-fold CV exercise, the model is fitted once over four partitions of the

modelling data, then tested on the fifth unseen partition. This is done five times, with

a different unseen partition of data tested each time. The metric used to assess

model performance here is the total Poisson deviance, where a lower deviance on

the unseen partition is preferred. The ‘pinball score’ of the best neural net model,

and of the GLM, is also shown for each partition. This score is essentially the

percentage reduction in deviance from a null model to the model of interest.

We can see that the total Poisson deviance of CANN and LocalGLMnet are about

the same, and are winning the race in terms of that metric. They are followed up by

the FFNN, with the GLM coming in last. Most notably, the pinball score of the neural

nets is approximately three times better than that of the GLM, over each unseen

partition.

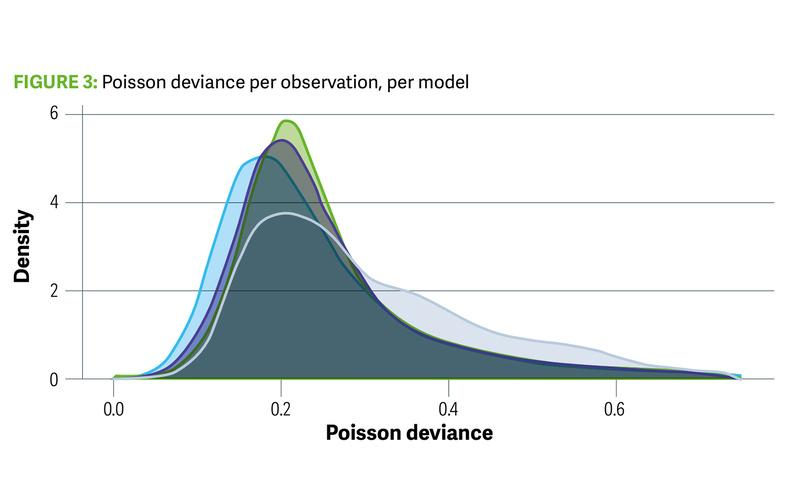

We have looked at the total Poisson deviance, but we can look at the full distribution

of values for each model as well. This is shown in the Figure 3, where we can see

that the GLM model has its weight of deviances further from 0 when compared with

the net models (CANN, FFNN, LocalGLMnet). LocalGLMnet appears to do best by

this measure.

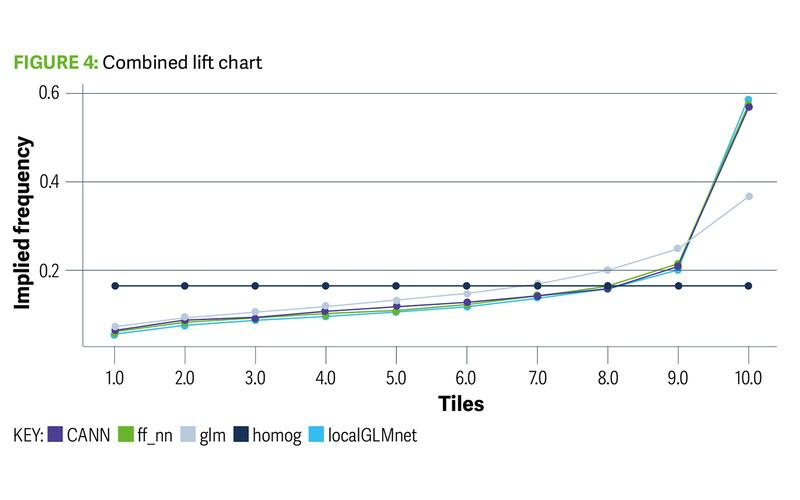

Using a lift chart, we can assess how well these model architectures distinguish

between high and low-risk policies. Figure 4 separates policies along the x axis in

deciles, according to how risky the respective models view those policies. For

example, the first decile contains the policies whose GLM prediction is in the lowest

10% of policies for that model. The first decile also contains the policies whose

prediction of frequency is in the lowest 10% for each of the FFNN, CANN and

LocalGLMnet models. Then, for each model’s lowest decile of policies, we calculate

the actual average observed frequency and plot this point. This is calculated and

plotted for all 10 deciles. The model that is best at distinguishing between low and

high risk policies will then have the greatest lift between the low and high deciles in

the chart. In Figure 4 we can see that neural network models are more successful at

this task than a GLM.

What does it mean for pricing?

It appears these newer architectures have more predictive power than legacy

models. As other studies have found, sacrifices are made in terms of transparency

and explainability when departing from GLM architecture, so explainable artificial

intelligence (XAI) may be required to help with model interpretation. However,

LocalGLMnet makes progress in this area where a local GLM structure is retained.

The CANN could also be a useful concept for insurers that have already developed a

GLM, as the neural network that is combined with the GLM may reveal opportunities

for further model refinement.

We should note that the results and conclusions here are somewhat specific to the

dataset used and the particular implementation of the models. If the GLM model

were optimised further, it is possible that we could observe different results.

The new technologies covered in this study may present a distinct edge in the

competitive world of insurance pricing. However, the care and skill of forward-

thinking and dynamic pricing teams will be required to steer these technologies

towards a podium finish.

The IFoA Actuarial Data Science Working Party would like to credit for their

original development and research on these architectures: Mario V Wüthrich,

Michael Merz and Jürg Schelldorfer for CANN; Ronald Richman and Mario V

Wüthrich for LocalGLMnet.

Karol Gawlowski is a predictive modeller at Allianz Commercial and chair of the

IFoA Actuarial Data Science Working Party

John Condon is a lecturer in actuarial science, School of Mathematical Sciences,

University College Cork

Jack Harrington is a senior pricing actuary at AXA Insurance

Davide Ruffini is a pricing actuary at AmTrust Assicurazioni in Milan

Image credit: Shutterstock

Enjoyed this read?

This article was originally published in The Actuary, March 2024 issue

https://www.theactuary.com/2024/03/05/gladiators-ready-pricing-models-fight-it-out

Head over theactuary.com for more insightful content.