Pricing in Retail Insurance: The Hidden Engine of Profitability

Pricing is often described as a technical task — something actuaries or data scientists solve with statistical models.

In reality, pricing is one of the most strategic decisions an insurance company makes.

Every price must balance several competing forces:

- Customer perception of fairness

- Portfolio profitability

- Competitive pressure

- Distribution dynamics

- Regulatory constraints

When pricing goes wrong, the consequences appear quickly.

Price too low and the portfolio attracts adverse selection while margins erode.

Price too high and conversion rates collapse, slowing growth and weakening market position.

In today’s retail insurance markets — shaped by aggregators, digital distribution, and embedded insurance models — pricing has become one of the primary levers of business performance.

Yet despite its importance, pricing is frequently misunderstood. Many teams focus heavily on building predictive models while overlooking the broader system in which pricing decisions actually operate.

The reality is simple:

Pricing is not a model. Pricing is a workflow.

In many pricing discussions, the focus immediately shifts to modelling techniques:

- Generalized Linear Models (GLMs)

- Gradient Boosting Machines (GBMs)

- Generalized Additive Models (GAMs)

- Other machine learning approaches

But a predictive model is only one component of the pricing process.

A robust pricing system must answer a set of interconnected questions:

- What business objective are we trying to achieve?

- What factors drive customer behaviour?

- How sensitive are customers to price changes?

- How should price recommendations be implemented in practice?

In regulated industries such as insurance, these questions are not optional. Pricing decisions must be:

- Understandable

- Explainable

- Defensible

— both internally and to regulators.

A well-designed pricing workflow typically follows several stages.

1. Define Business Objectives

Pricing strategies may aim to:

- Improve profitability

- Accelerate growth

- Optimise portfolio mix

- Increase customer retention

Without a clear objective, even the best model cannot produce meaningful pricing decisions.

2. Prepare and Understand Data

Data preparation strongly influences pricing outcomes.

Key elements include:

- segmentation design

- feature engineering

- behavioural data integration

The quality of this step determines whether the model reflects real-world customer behaviour.

3. Build Predictive Models

Predictive modelling estimates quantities such as:

- risk (expected loss)

- demand

- conversion and retention probability

But modelling alone does not create business value.

The real impact begins when we move to the next stage: understanding price sensitivity.

Elasticity: The Heart of Pricing Behaviour

At the core of any pricing system lies one critical concept: price elasticity.

Elasticity measures how customer demand responds to price changes. It determines how conversion or retention rates evolve when prices increase or decrease.

Many practitioners are comfortable building predictive models. Far fewer fully understand how their models behave when the “price knob” is turned.

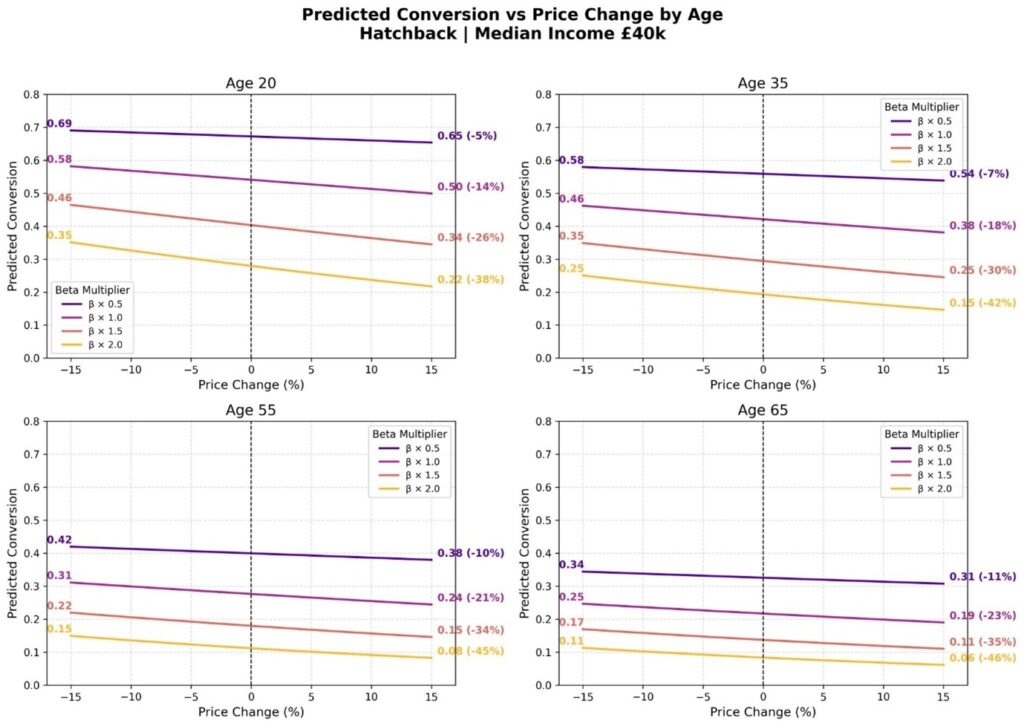

Consider a simplified example: a GLM predicting conversion probability for motor insurance.

A typical model output might include coefficients such as:

- Intercept: 1.2432 (baseline conversion)

- Vehicle Type – Hatchback: 0.2155

- Vehicle Type – SUV: -0.7363

- Vehicle Type – Sedan: 0.6525

- Vehicle Type – Sports Car: 0.3883

- Age: -0.0321

- Income: 1.11E-05

- Price: -1.1101

Among these parameters, the price coefficient is the most important.

It determines how sensitive customers are to price changes and therefore drives the entire pricing engine.

But interpreting elasticity requires more than simply reading coefficients.

To truly understand how a model behaves, we must simulate price movements and observe how predicted conversion or retention evolves.

For example as the graph shows, by analysing predicted conversion across a range of –15% to +15% price changes, we can visualise how different customer segments respond.

These simulations often reveal valuable insights.

You may discover that younger drivers have a higher baseline conversion rate than older drivers. But this raises an important question:

Are they less price-sensitive, or are they simply offered more competitive prices?

Elasticity stress testing also helps evaluate how robust the model is.

If we scale the price coefficient — for example multiplying it by values between 0.5 and 2.0 — we can observe how aggressive or conservative the pricing engine becomes.

- If elasticity is overestimated, optimisation engines become overly cautious and leave money on the table.

- If elasticity is underestimated, the optimiser may push prices too aggressively, creating both commercial and regulatory risks.

This highlights a fundamental principle of pricing:

Any bias embedded in the model will be inherited by the pricing engine.

If a model incorrectly estimates elasticity for a specific segment, the optimiser will systematically misprice that group.

For this reason, interpreting elasticity is just as important as building the model itself.

When Machine Learning Meets Pricing

Over the past decade, machine learning techniques — particularly Gradient Boosting Machines (GBMs) — have become increasingly popular in insurance analytics.

These models capture complex nonlinear relationships across large numbers of variables and often deliver strong predictive performance.

However, applying them directly to pricing introduces a hidden challenge.

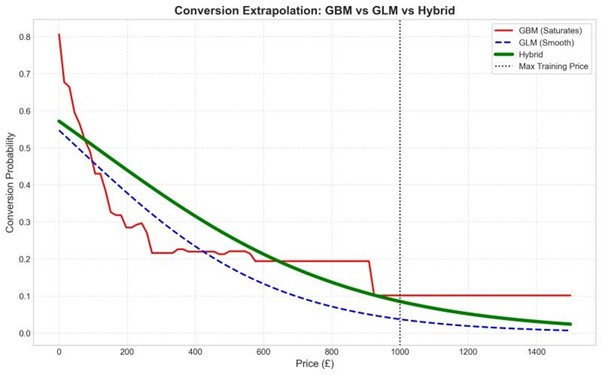

Tree-based models such as GBMs divide the data into discrete regions. When a price change moves outside the ranges observed during training, the model may lose sensitivity.

In practice, this means the predicted relationship between price and conversion can become flat.

This phenomenon is sometimes referred to as price saturation (see red line in the below graph).

When the model stops reacting to price increases, optimisation engines may interpret this as evidence that demand is insensitive to price — effectively suggesting that margin is “free”.

This can lead to unrealistic and risky pricing recommendations.

The problem does not only occur at the extremes of the data. It can also appear in areas where the dataset contains relatively few observations, producing plateau-like behaviour where the model stops responding to price changes.

Why GLMs Alone Are Not Enough

A natural response to this issue is to rely exclusively on GLMs.

Because GLMs impose a parametric structure, they produce smooth and interpretable relationships between price and demand (see blue dotted line in the below graph).

This makes them well suited for modelling elasticity.

However, GLMs also have limitations.

Retail insurance pricing involves complex interactions between many risk factors:

- Geography

- Vehicle characteristics or other lines characteristics

- Customer demographics

- Behavioural variables and more

Capturing these nonlinear relationships using a simple parametric structure can be difficult.

As a result, pure GLM approaches may sacrifice predictive power in risk segmentation.

In other words, the model may produce a beautiful price curve applied to an imperfect understanding of risk.

Instead of choosing between interpretability and predictive performance, many modern pricing systems combine both.

One particularly architecture is the hybrid GBM–GLM model.

This approach separates the modelling of risk from the modelling of price behaviour (see green line in the below graph).

Step 1 — Capture Complex Risk Patterns

A GBM model captures nonlinear interactions among risk features.

Rather than producing the final prediction directly, the model generates a risk offset summarising these interactions.

Step 2 — Model Price Behaviour Explicitly

This offset is then passed into a parametric GLM.

The GLM explicitly models price and behavioural variables, ensuring a smooth and economically meaningful elasticity curve.

The result is a system that combines:

- the predictive strength of machine learning

- the interpretability of parametric models

- stable price elasticity suitable for optimisation

- improved transparency for regulators and stakeholders

This architecture allows pricing systems to maintain economic logic while benefiting from modern predictive methods.

The Ethical Responsibility of Pricing

Pricing decisions do not exist in a purely technical vacuum.

In retail insurance, they also carry ethical and regulatory implications.

It is easy to focus on predictive performance and margin improvement. But responsible pricing requires a broader perspective.

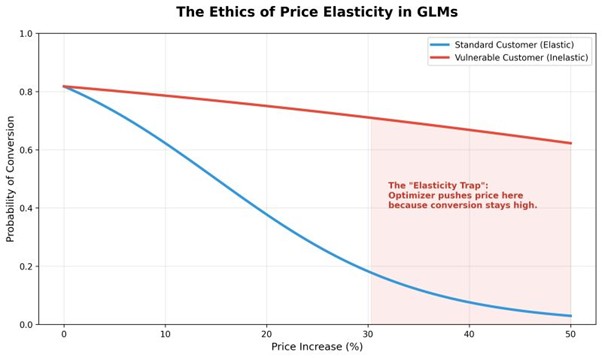

Some customer segments may appear highly inelastic. In many cases this reflects circumstances rather than genuine willingness to pay — for example when individuals urgently need insurance coverage.

Treating such segments as opportunities for aggressive pricing can create serious fairness concerns.

Responsible pricing frameworks therefore require careful oversight.

Variables prohibited by regulation — such as:

- gender

- ethnicity

- disability

— must be excluded from models regardless of their predictive value.

Beyond formal regulation, analysts should also examine their models critically. Coefficients that contradict real-world behaviour may signal hidden biases in the data.

Elasticity assumptions should also be treated cautiously.

From both an ethical and regulatory standpoint, it is often safer to assume slightly higher price sensitivity (pushing the red curve especially for vulnerable customer towards the blue line) than to risk systematic overpricing of vulnerable groups.

Once optimisation engines are deployed, they will relentlessly pursue the objectives encoded in the model.

A pricing system that ignores fairness may produce short-term profit — but it will not remain sustainable.

From Models to Real Pricing Decisions

Ultimately, the goal of pricing analytics is not to build sophisticated models.

The goal is to make better pricing decisions.

Achieving this requires understanding how all elements of the pricing workflow interact:

- business objectives

- data preparation

- predictive modelling

- elasticity estimation

- optimisation

- regulatory constraints

Only when these components work together can pricing systems deliver sustainable performance improvements.

Mastering this process requires more than technical modelling skills.

It requires learning how to think like a pricing strategist.

Learning Practical Pricing in Insurance

To help practitioners develop these skills, I recently created a Retail Insurance Pricing Masterclass focused on how pricing works in real-world environments.

The course covers topics such as:

- translating business objectives into data-driven pricing models

- building pricing models in Python

- measuring and stress-testing elasticity

- applying fairness and regulatory constraints in practice

- designing hybrid GBM–GLM pricing architectures

- designing an optimisation workflow step by step

The focus is not just on building models, but on designing pricing systems that can be understood, explained, and defended.

Learn more about the course here:

https://learn.insurancepricingmodelling.com

By Cosimo Morfeo, insurance pricing specialist

#priceoptimisation #insurancepricing #priceelasticity